First-Time Home Buyers: A Guide to Navigating the Homeownership Process Buying your first home can be an exciting and daunting experience. As a first-time homebuyer, it's essential to know the necessary steps and responsibilities that come with owning a home. This article will provide a helpful guide for those looking to embark on their first homeownership journey. Financial Preparedness Before beginning your search for a new home, it's crucial to assess your financial readiness. Budgeting and saving for a down payment is a necessary first step to ensuring that you can afford the home you want. Knowing the different mortgage rates and types can also help you choose the one that best fits your financial situation. Additionally, don't forget to factor in closing costs, which can add up quickly and take you by surprise. Home Selection Once you are financially prepared, it's time to determine what you need and want in a home. Consult with a reputable real estate agent to help you navigate the home buying process. Work with them to do in-depth research on properties to make sure you find the one that best suits your needs. Home Inspection After finding your dream home, it's important to have it inspected by a professional home inspector. Home inspections are essential to uncover any hidden problems that may not be visible to the untrained eye. Understanding the inspection report can help you make informed decisions when it comes to negotiating the price or even walking away from the deal. Closing the Deal Negotiating the price is an essential part of the home buying process. Make sure you understand all of the contracts and paperwork involved and know what to expect at closing. Don't be afraid to ask questions and seek clarification on anything you don't understand. Conclusion To summarize, being a first-time homebuyer requires financial preparedness, careful home selection, professional home inspection, and savvy negotiation skills. It's essential to continue learning about homeownership and staying up-to-date on any changes in the market. Ultimately, owning a home can be a rewarding experience, and with the right preparation, you can make the most of it.

Northern Colorado Real Estate Search

Northern Colorado Real Estate and Community News

what are some common mistakes to avoid when buying a house

Buying a home is an exciting event for many people. However, it can also be quite overwhelming, as there are many factors to consider before making such a big investment. Whether you're a first-time homebuyer or have bought a home before, it's important to avoid certain mistakes that could end up costing you a lot of time, money, and stress in the long run. Setting a budget is one of the most important things to consider before buying a home. Not having a budget in place could result in overspending, causing you to be saddled with debt or ending up with a home that you cannot afford. To avoid this mistake, be sure to set a realistic budget that takes into account all expenses related to the purchase, such as closing costs, mortgage payments, and utility bills. Additionally, consider hiring a financial advisor to help you create a budget that works for you. Skipping the inspection process is another mistake that can be costly. A thorough inspection can uncover potential issues with the home, such as mold, water damage, or faulty wiring. Not having an inspection could result in expensive repairs down the line, leaving you with a home that costs much more than you bargained for. To ensure you have a complete inspection, hire a qualified inspector and be present during the inspection to ask questions and address any concerns. Another mistake to avoid is not researching the neighbourhood where you're considering buying a home. The neighbourhood can have a huge impact on your quality of life, so it's important to research the community, schools, amenities, and safety records before making a purchase. Not doing so could result in a home that's in an undesirable location or doesn't fit your lifestyle needs. Thinking about the future is also important when buying a home. Not considering your future needs, such as the size of your family or potential job changes, could leave you with a home that no longer suits your needs a few years down the line. To avoid this, think about your long-term goals and consider how a potential home fits into those plans. To recap, common mistakes to avoid when buying a home include not setting a budget, skipping the inspection, not researching the neighbourhood, and not considering the future. By avoiding these mistakes and following the tips provided, you'll be on your way to successful home buying. Remember, taking the time to carefully consider your purchase can save you time, money, and stress in the long run.

Selling your home by owner in colorado

Selling Your Home: An Explainer Guide for Owners Selling a home can be a daunting task, especially if it’s your first time doing so. But with the right knowledge and preparation, it can be a smooth and exciting process. One option for homeowners is to sell their home by owner instead of using a real estate agent. This not only saves on commission fees but also gives the seller more control over the process. Here’s a handy guide to help homeowners understand what’s involved in selling their home independently and make the most of their investment. Preparing the Home The first step in selling your home is to make sure it’s ready to be shown to potential buyers. This means giving it a proper cleaning and presentation. A clean and clutter-free home can go a long way in making a good first impression. Don't underestimate the power of small repairs and maintenance, as they can help increase the value of the home. Fixing any leaky faucets, painting the walls, and replacing outdated light fixtures can make a big difference in how your home shows to buyers. Setting the Price Pricing your home correctly is key to attracting the right buyers. It involves researching the market to get an idea of what similar homes are selling for in the area. It’s important to strike a balance between pricing it competitively and not leaving money on the table. Understanding the value of the home is also important. This includes factors such as the location, the condition of the property, and any recent upgrades or renovations. Marketing the Home Now that your home is ready and priced correctly, it’s time to market it. Advertising in local newspapers and magazines can be a good start. Online listings, such as Zillow and Realtor.com, are other important avenues to reach potential buyers. Social media platforms like Facebook and Instagram are also popular places to showcase your home. Make sure to take high-quality photos and videos that showcase the best features of the property. Closing the Deal Once you have an interested buyer, it’s time to start negotiations. It’s important to be clear on what you’re selling and what’s included in the sale. This includes any fixtures, appliances, and furniture. Negotiating the price and any other conditions of the sale can take some time, but staying positive and being patient can help make the process smoother. Once an agreement is reached, it’s important to finalize the sale by drafting a purchase agreement and arranging for an inspection and closing. Conclusion Selling your home by owner takes effort and patience, but it can be a rewarding process. Preparing your home, setting the price, marketing it, and closing the deal are all important steps to consider. Remember to stay positive and communicate clearly with potential buyers. By following these steps, homeowners can successfully sell their homes independently and make the most of their investment.

Buying a home in Colorado

If you've been thinking about purchasing a home, now is the time to make your move! Home ownership is incredibly important for a number of reasons, and there are plenty of great benefits that come along with buying a home in Colorado. First and foremost, owning a home gives you a sense of pride and accomplishment. It's a major investment and a symbol of your success, and it's a place where you can truly make your mark and create memories that will last a lifetime. But beyond that, buying a home in Colorado can be a savvy financial move as well. Your mortgage payment will likely be less than what you would pay in rent for a comparable property, and you'll be building equity and increasing your net worth in the process. So, if you're ready to take the plunge and purchase a home in Colorado, here's what you need to know: Determine Your Budget The first step in buying a home is to evaluate your financial situation and determine what you can afford. You'll want to take a close look at your income, expenses, and other financial obligations to come up with a realistic budget. Once you have an idea of what you can afford, it's a good idea to get pre-approved for a mortgage loan so you can start shopping with confidence. Find The Right Location Once you know how much you can afford to spend, it's time to start looking for the right location. Colorado is home to a wide variety of unique and beautiful neighborhoods, so take the time to research your options. Consider factors like proximity to work, schools, and other amenities, and make sure you're selecting a location that fits your lifestyle. Hire A Realtor Working with a licensed real estate agent is key to finding the perfect home in Colorado. A good agent will help you identify homes that match your criteria, and they'll be able to provide valuable insights into the local real estate market. Make sure you find an agent who you feel comfortable working with and who has experience in the Colorado market. Make An Offer and Close The Deal Once you've found the home of your dreams, it's time to make an offer and close the deal. Your agent will help you submit a formal offer on the property, and once it's accepted, you'll need to complete the necessary paperwork and secure financing. Finally, you'll close on the home and take possession, officially becoming a homeowner in beautiful Colorado. So, there you have it - a quick rundown of what to expect when buying a home in Colorado. With a little bit of planning and preparation, you'll be able to find the perfect property and start enjoying all the benefits of home ownership in no time. Good luck!

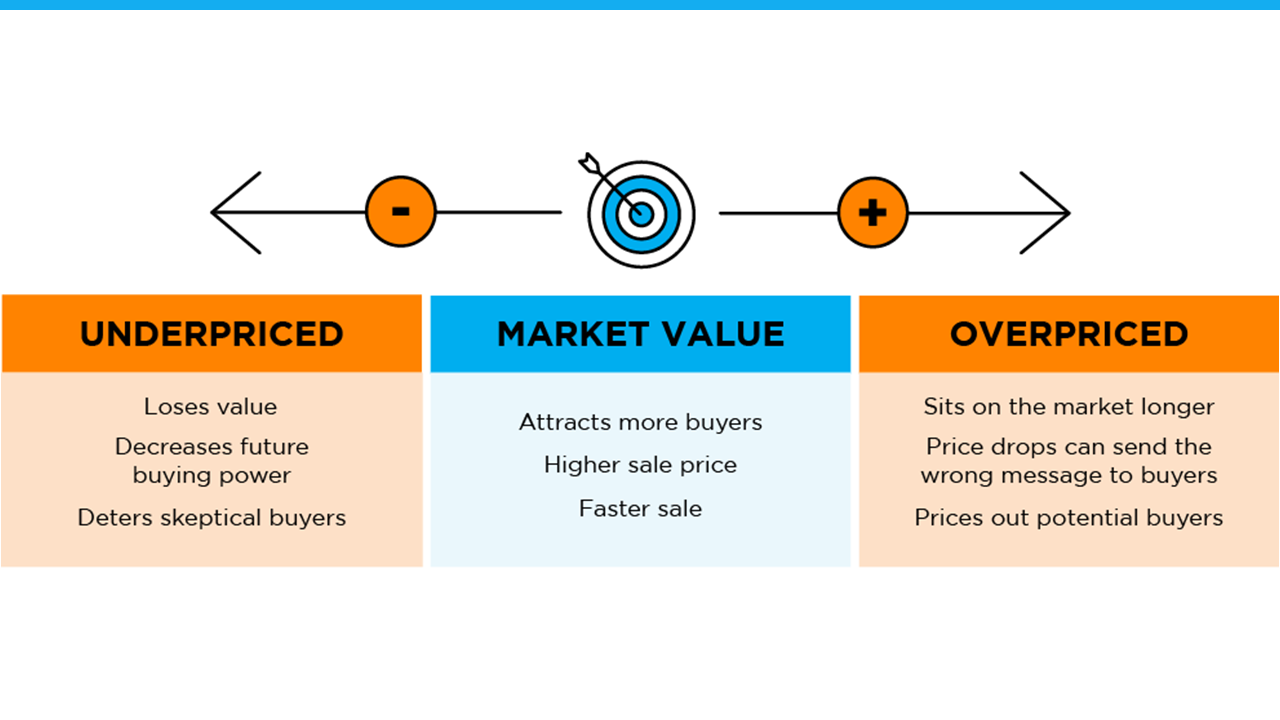

Want To Sell Your House This Spring? Price It Right.

Over the last year, the housing market’s gone through significant change. While it’s still a sellers’ market, homes that are priced right are selling, and they get the most attention from buyers right now. If you’re thinking of selling your house this spring, it’s important to lean on your expert real estate advisor when it comes to setting a list price. As Realtor.com explains:

“Move-in-ready homes with curb appeal and in desirable areas—and that are priced to sell—are especially likely to move quickly this spring.”

In today’s market, how you price your house will not only make a big difference to your bottom line, but to how quickly your house will sell.

Why Pricing Your House Right Matters

Your asking price sends a message to potential buyers, especially today.

If it’s priced too low, you may leave money on the table or discourage buyers who may see a lower-than-expected price tag and wonder if that means something is wrong with the home.

If it’s priced too high, you run the risk of deterring buyers. When that happens, you may have to lower the price to drive interest when your house sits on the market for a while. But be aware that a price drop can be seen as a red flag by some buyers who will wonder what it means about the home.

To avoid either headache, price it right from the start. A real estate professional knows how to determine the ideal asking price. They balance the value of homes in your neighborhood, current market trends, buyer demand, the condition of your house, and more to find the right price. This helps lead to stronger offers and a greater likelihood your house will sell quickly.

The visual below helps summarize the impact your asking price can have:

Bottom Line

Homes priced at the current market value are selling faster and at a better price right now. To make sure you price your house appropriately, maximize your sales potential, and minimize your hassles, let’s connect today.

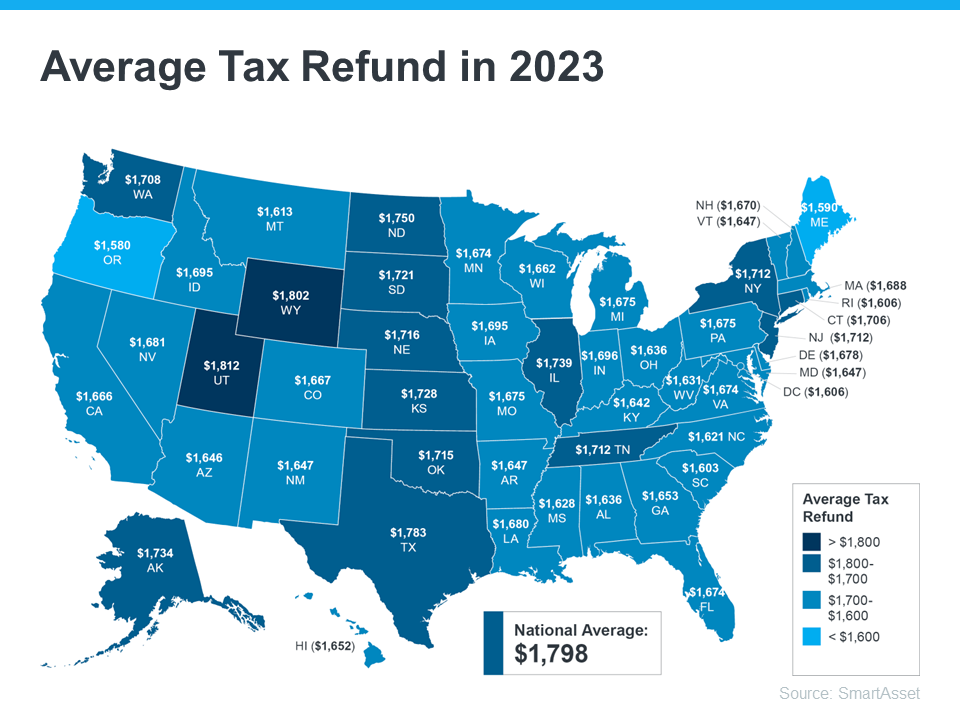

Your Tax Refund Can Help You Achieve Your Homebuying Goals

Have you been saving up to buy a home this year? If so, you know there are a variety of expenses involved – from your down payment to closing costs. But there’s good news – your tax refund can help you achieve your goals by paying for some of these expenses.

SmartAsset estimates the average American will receive a $1,798 tax refund this year. The map below provides a more detailed estimate by state:

According to Freddie Mac, there are multiple ways your refund check can help you as a homebuyer. If you’re getting a refund this year and thinking about buying a home, here are a few tips to keep:

- Saving for a down payment – One of the largest barriers to homeownership is saving for a down payment. You could reach your savings goal more quickly than expected by using your tax refund to help with your down payment.

- Paying for closing costs – You have to pay fees to your lender, real estate agent, and other parties involved in the homebuying transaction before you can officially take ownership of your home. You could direct your tax refund toward these closing costs.

- Lowering your interest rate – Your lender might give you the option to buy down your mortgage interest rate during the homebuying process. That means, you could pay upfront to have a lower interest rate on your fixed-rate mortgage.

The best way to prepare to buy a home is to work with a trusted real estate professional who understands the process. They’ll help you navigate the costs you may encounter as you begin your homebuying journey.

Bottom Line

Your tax refund can help you reach your goals of homeownership. Let’s connect to discuss how you can start your journey today.

The Big Advantage If You Sell This Spring

Thinking about selling your house? If you’ve been waiting for the right time, it could be now while the supply of homes for sale is so low. HousingWire shares:

“. . . the big question is whether we are finally starting to see the seasonal spring increase in inventory. The answer is no, because active listings fell to a new low last week for 2023 . . .”

The National Association of Realtors (NAR) confirms today’s housing inventory is low by looking at the months’ supply of homes on the market. In a balanced market, about a six-month supply is needed. Anything lower is a sellers’ market. And today, the number is much lower:

“Total housing inventory registered at the end of February was 980,000 units, identical to January and up 15.3% from one year ago (850,000). Unsold inventory sits at a 2.6-month supply at the current sales pace, down 10.3% from January but up from 1.7 months in February 2022.”

Why Does Low Inventory Make It a Good Time To Sell?

The less inventory there is on the market when you sell, the less competition you’re likely to face from other sellers. That means your house will get more attention from the buyers looking for a home this spring. And since there are significantly more buyers in the market than there are homes for sale, you could even receive more than one offer on your house. Multiple offers are on the rise again (see graph below):

If you get more than one offer on your house, it becomes a bidding war between buyers – and that means you have greater leverage to sell on your terms. But if you want to maximize the opportunity for a bidding war to spark, be sure to lean on your expert real estate advisor. While we’re still in a strong sellers’ market, it isn’t the frenzy we saw a couple of years ago, and today’s buyers are focused on the houses with the greatest appeal. Clare Trapasso, Executive News Editor at Realtor.com, explains:

"Well-priced, move-in ready homes with curb appeal in desirable areas are still receiving multiple offers and selling for over the asking price in many parts of the country. So, this spring, it's especially important for sellers to make their homes as attractive as possible to appeal to as many buyers as possible.”

Bottom Line

If you’ve been waiting for the right time to sell your house, low inventory this spring sets you up with a big advantage. Let’s connect today to make sure your house is ready to sell.

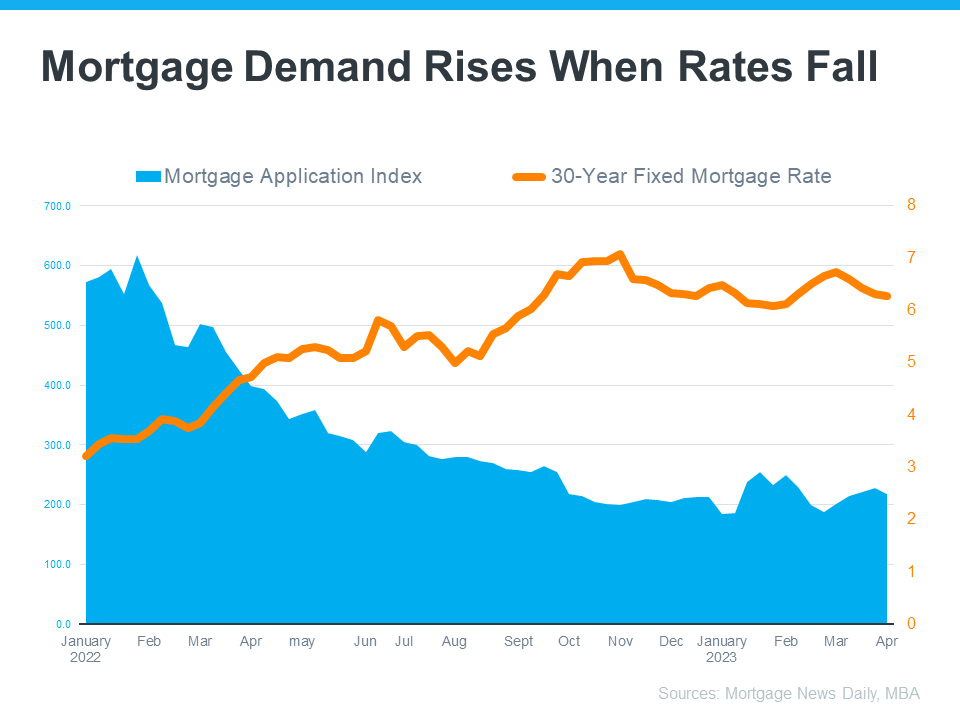

Homebuyer Activity Shows Signs of Warming Up for Spring

The spring season appears to be warming up in housing as more and more buyers enter the market. And after rising mortgage rates sidelined so many buyers last year, that’s a good sign for sellers. Realtor.com has the latest:

“Spring is officially here, and like green shoots emerging from the bleak winter, new data suggests that more buyers are back in the market, although more subdued compared to a year ago.”

We know buyer activity is trending up because of mortgage purchase application data. According to Investopedia:

“A mortgage application is a document submitted to a lender when you apply for a mortgage to purchase real estate.”

That means the number of mortgage applications shows how many buyers are applying for mortgages. Put another way, an increase in mortgage applications means an increase in buyer demand – and as Joel Kan, VP and Deputy Chief Economist at the Mortgage Bankers Association (MBA), explains, application activity started ramping up as mortgage rates fell steadily in March:

“Application activity increased as mortgage rates declined . . . recent increases, along with data from other sources showing an uptick in home sales, is a welcome development.”

In fact, we can see how mortgage rates have a direct impact on applications over time. As rates rose dramatically last year, applications fell in response (see graph below):

The recent uptick in mortgage applications, as well as the decline in mortgage rates, is good news for sellers because it means more buyers are actively looking for homes.

What This Means for You

Buyers are coming this spring, which is typically the busiest time of the year in real estate. And as Realtor.com tells us, if you’re a seller, you need to prepare:

“If homeowners are planning to sell in 2023, now is the time to get ready.”

The means working with a local real estate agent to maximize your home’s appeal and get it listed at the ideal price for your area.

Bottom Line

The housing market is warming up for spring. If you’re thinking about selling your house and taking advantage of this recent uptick in buyer activity, let’s connect.

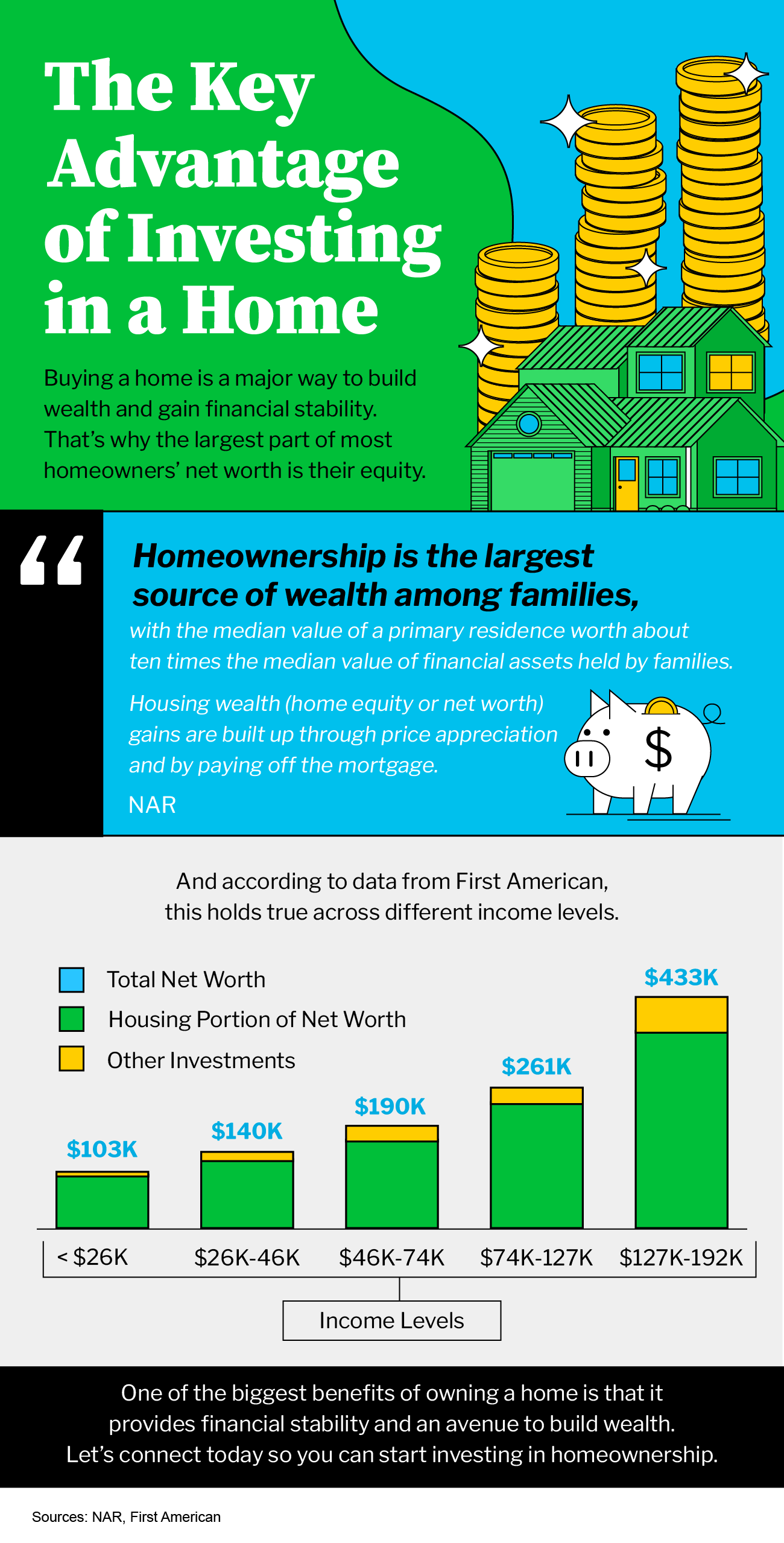

Trying To Buy a Home? Hang in There.

We’re still in a sellers’ market. And if you’re looking to buy a home, that means you’re likely facing some unique challenges, like difficulty finding a home and volatile mortgage rates. But keep in mind, there are some benefits to being a buyer in today’s market that give you good reason to stick with your search. Here are a few of them.

Long-Term Benefits Outweigh Short-Term Challenges

Owning a home grows your net worth – and since building that wealth takes time, it makes sense to start as soon as you can. If you wait to buy and keep renting, you’ll miss out on those monthly housing payments going toward your home equity. Freddie Mac puts it this way:

“Homeownership not only builds a sense of pride and accomplishment, but it’s also an important step toward achieving long-term financial stability.”

The key there is long-term because the financial benefits homeownership provides, like home value appreciation and equity, grow over time. Those benefits are worth the short-term challenges today’s sellers’ market presents.

Mortgage Rates Are Constantly Changing

Mortgage rates have been hovering around 6.5% over the last several months. However, as Sam Khater, Chief Economist at Freddie Mac, notes, they’ve been coming down some recently:

“Economic uncertainty continues to bring mortgage rates down. Over the last several weeks, declining rates have brought borrowers back to the market . . .”

Lower mortgage rates improve your purchasing power when you buy, and that can help make homeownership more affordable. Hannah Jones, Economic Data Analyst at realtor.com, explains:

“As we move into the spring buying season, mortgage rates have ticked lower, a welcomed sign of progress towards affordability.”

The recent drop in mortgage rates is good news if you couldn’t afford to buy a home when they peaked.

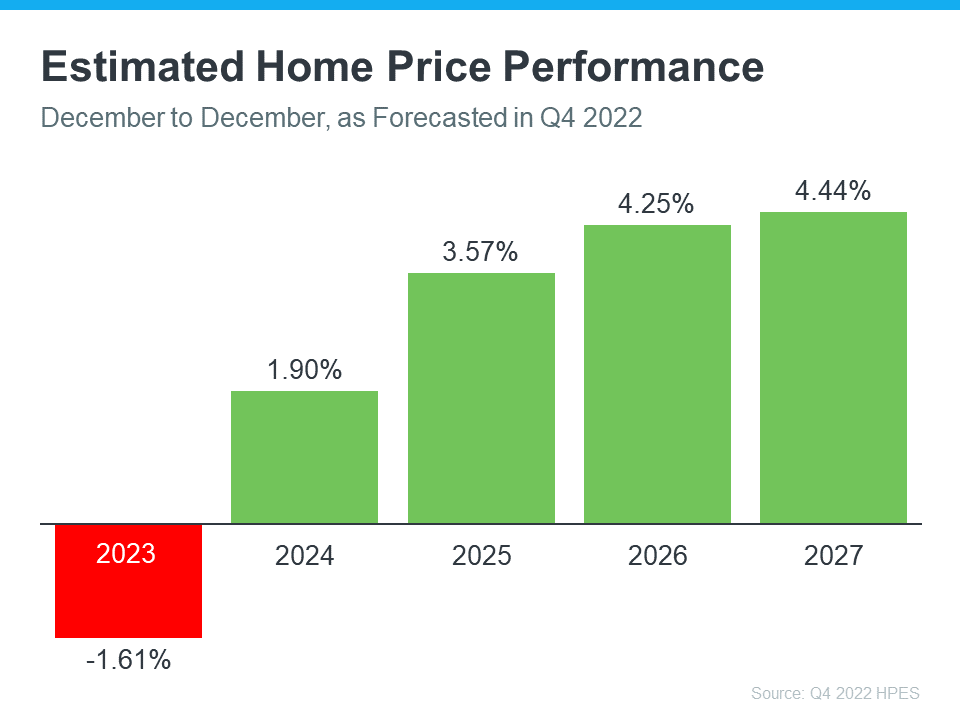

Home Prices Will Increase

According to the Home Price Expectation Survey, which polls over 100 real estate experts, home values will go up steadily over the next few years after a slight decline this year (see graph below):

Rising home prices in the coming years means two things for you as a buyer:

- Waiting to buy a home could mean it’ll become more expensive to do so.

- Buying now means the value of your home, and your net worth, will likely grow over time.

Bottom Line

If you’ve been trying to buy a home, hang in there. Mortgage rates have ticked down some recently, home prices are forecast to increase in the coming years, and the long-term benefits of homeownership outweigh many of the short-term challenges.